When it’s time for your commercial policy renewal review, you might feel overwhelmed by all the details and decisions ahead. But this moment is crucial—it’s your chance to ensure your business stays protected without paying for coverage you don’t need.

Are you confident your current policy truly matches your evolving business risks? Or could there be gaps that put you at risk of costly surprises? You’ll discover simple, practical steps to review your commercial insurance policy effectively. You’ll learn how to spot important changes, communicate with your insurer, and secure the best coverage for your business’s unique needs.

Don’t leave your protection to chance—read on and take control of your commercial policy renewal today.

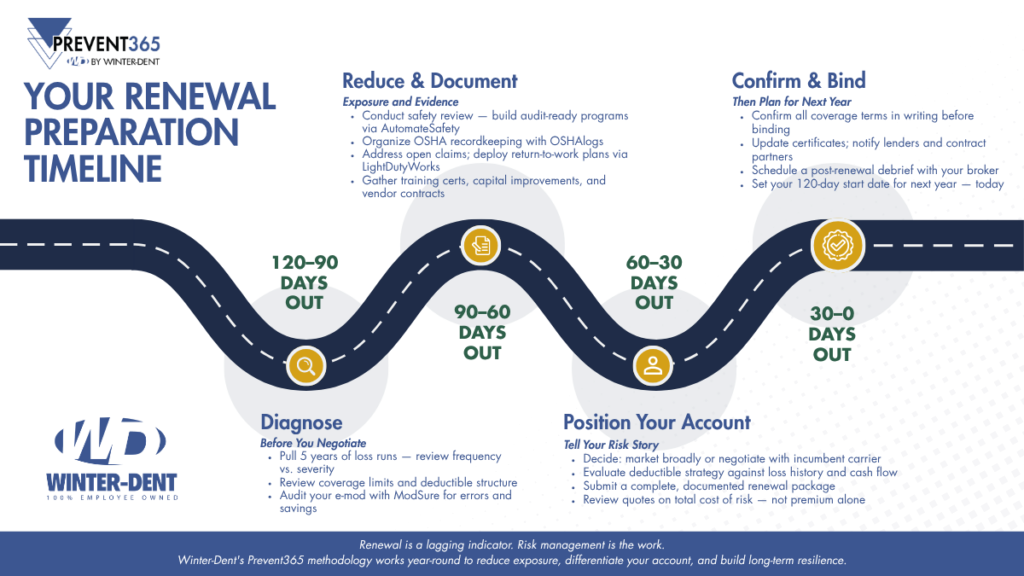

Renewal Timeline

Key dates help keep your commercial policy renewal on track. Start by noting the policy expiration date. Most insurers send a renewal notice 30 to 60 days before this date. This notice gives time to review and make changes.

Mark the notification period for any adjustments or cancellations. This period often requires written notice 15 to 30 days before renewal. Missing this deadline may cause automatic renewal without changes.

Keep a calendar with these important dates:

| Date Type | Typical Time Frame | Action Required |

|---|---|---|

| Policy Expiration | Day 0 | Renew policy or make changes |

| Renewal Notice | 30-60 days before expiration | Review policy details |

| Notification Period | 15-30 days before expiration | Submit changes or cancellation |

Tracking these dates ensures you do not miss important steps. Staying organized helps avoid unexpected coverage gaps.

Policy Review

Coverage limits define the maximum amount an insurer will pay. Exclusions list what is not covered by the policy. Both are key to understanding protection.

Identify any gaps where your business may lack coverage. For example, new equipment or services might not be included. Gaps can leave you financially exposed.

Look for overlaps where coverage duplicates. Overlaps can cause you to pay more than needed. Removing overlaps helps lower premium costs.

| Aspect | Importance | Action |

|---|---|---|

| Coverage Limits | Defines maximum payout | Check if limits meet business needs |

| Exclusions | Lists what is not covered | Understand exclusions carefully |

| Gaps | Areas lacking coverage | Identify and add missing coverage |

| Overlaps | Duplicate coverage areas | Remove overlaps to reduce costs |

Business Changes

Changes in your business can affect your insurance coverage needs. Growing operations or new services may need extra protection. Downsizing or selling parts might mean less coverage is necessary.

Review your policy to match current business activities. Make sure all important assets and risks are included. Update details like address, ownership, and employee numbers to keep the policy accurate.

Accurate policy information helps avoid coverage gaps or unnecessary costs. Inform your insurer promptly about any changes. This ensures your business stays properly protected and compliant with policy terms.

Communication Strategies

Proactive client outreach helps keep communication clear and timely. Agents should contact clients before the renewal date. This builds trust and allows clients to ask questions early. Regular phone calls and emails keep clients informed about any policy changes or updates. It also helps spot any new risks or coverage needs.

Agent and insurer collaboration ensures smooth policy renewal. Agents and insurers must share information quickly. Clear roles and responsibilities help avoid confusion. Working as a team speeds up the process and improves service quality. Both parties should update each other about client feedback and policy adjustments.

Maximizing Savings

Discount opportunities can greatly reduce your renewal costs. Many insurers offer savings for bundling policies or having a clean claims record. Ask about discounts for early renewal or paying annually. Small changes in coverage might also unlock better rates.

Comparing renewal offers is key. Review every offer carefully. Check the coverage limits, deductibles, and exclusions. Don’t just look at price; consider what is included. Sometimes a higher premium means better protection.

| Factor | What to Check |

|---|---|

| Premium | Compare total cost for the year |

| Coverage | Limits and types of protection offered |

| Deductible | Amount you pay before insurance pays |

| Discounts | Available savings options and eligibility |

Coverage Optimization

Tailoring policies means matching coverage to specific business risks. Every business has unique threats that need special attention. Policies should reflect changes in operations, location, or staff size to stay effective.

Avoiding coverage gaps is crucial. Gaps can lead to unexpected costs if a claim is denied. Regularly reviewing policies helps find and fix these gaps before renewal. It also ensures no important risks are left uninsured.

Discussing your needs with an insurance agent can clarify complex terms. Agents help adjust limits and add endorsements to fit your business better. This process keeps your policy strong and relevant.

Automatic Renewal Insights

Automatic renewal happens when a policy extends without action from the insured. It often applies to commercial insurance policies that are set to renew on a specific date. The insurer usually sends a renewal notice 30 to 60 days before the expiration.

Risks of automatic renewal include missing changes in coverage or rates. Businesses might pay for unneeded coverage or miss better options. It can also cause surprises if claims history changes, leading to higher premiums.

Policies that renew automatically may not reflect the current needs of the business. Regularly reviewing policies before renewal helps avoid these risks. Communicating with your insurer ensures the coverage matches your business situation.

Claim History Effects

Claim history plays a big role in setting renewal terms. Insurance companies check past claims to decide your new policy price and coverage. Fewer claims usually lead to better renewal offers and lower premiums.

Keeping your claims record clean helps you save money. Fix problems quickly and avoid unnecessary claims. Use safety measures to reduce risks. This can improve your claims record over time.

Regularly review your policy and talk with your agent. Ask about ways to improve your claims history and lower costs. Good communication helps find the best renewal terms for your business.

Renewal Checklist

Start by gathering essential documents like your current policy, claim history, and business info. Check for any changes in your business that may affect coverage needs. Review the terms, limits, and exclusions of your existing policy carefully. Confirm the renewal date to avoid any gaps in coverage. Communicate with your insurance agent to discuss any updates or questions. Make sure to note any discounts or changes in premiums. Keep copies of all documents for your records. A clear timeline helps complete the renewal smoothly. Early preparation avoids last-minute stress. Staying organized ensures your business stays protected.

Leveraging Technology

Data-driven alerts help businesses track policy renewal dates. Automated systems send reminders before deadlines, reducing missed renewals. This ensures continuous coverage and avoids penalties.

Smart outreach tools allow insurers to contact clients efficiently. Personalized emails and texts keep clients informed and engaged. These tools save time and improve communication quality.

Frequently Asked Questions

What Does It Mean When Your Claim Is In Review?

When your claim is in review, the insurer is examining details to verify coverage and validate your claim’s legitimacy. This process ensures accurate decision-making and may take time.

Which Insurance Company Denies Most Claims?

Some reports show companies like State Farm and Allstate deny more claims, often due to stricter policy terms. Claim denial rates vary widely by region and policy type. Always review insurer reputation and customer feedback before choosing coverage.

Does Commercial Insurance Automatically Renew?

Commercial insurance may or may not renew automatically. It depends on your policy, insurer, and claims history. Usually, insurers notify you before renewal.

How To Write A Good Review For An Insurance Company?

Write a good insurance review by honestly describing your experience, service quality, and claims handling. Highlight responsiveness and policy clarity. Use clear, positive language. Include specific examples to build trust and help others make informed decisions. Keep it concise and genuine.

Conclusion

A commercial policy renewal review helps protect your business well. It ensures coverage fits your current needs and risks. Regularly check your policy details and limits carefully. Discuss any changes or concerns with your insurance agent. Staying informed can prevent gaps and costly surprises later.

Taking time now saves money and stress in the future. Keep your business secure with a clear renewal plan.